Reforms the business tax structure in San Francisco to increase the city’s economic resilience, adapt to post-COVID hybrid work patterns, create more transparency for taxpayers, and help small businesses.

Proposition M would reform the business tax structure in San Francisco to increase the city’s economic resilience, adapt to post-COVID hybrid work patterns, create more transparency for taxpayers, and help small businesses.

The city’s gross receipts tax rates and calculation methodology would change in the following ways:

Taxes would be calculated on the basis of gross receipts in San Francisco, with less weight on companies’ payroll in San Francisco (in contrast to the current system, which rewards companies that reduce the number of staff working in the city).

The number of tax schedules would drop from 14 to seven to make it easier for businesses to understand their costs and for the city to administer business taxes.

The Overpaid Executive Tax — a relatively risky source of revenue for the city because it comes from a small set of large employers — would be reduced by 80%.

The Homelessness Gross Receipts Tax would have new tax schedules, rates, and tiers to make it more consistent with the gross receipts tax and to distribute the tax burden on a wider range of industries. The total revenues dedicated for homeless services would remain unchanged.

The small business tax exemption would be expanded to businesses with gross receipts less than $5 million. Consequently, almost all restaurants in the city would be exempt.

The proposal would eliminate $10 million in licensing and registration fees that are a burden to small businesses, especially restaurants and bars.

The measure would delay and restructure previously scheduled tax increases approved by voters in 2020’s Proposition F.

According to the Office of the Controller, if the measure passes, the city’s tax collections would be reduced for three years by $40 million annually. The scheduled Prop. F increases would be implemented at the higher rates of 4% in 2027 and 3% in 2028, offsetting those losses from the first three years. After fiscal year 2029–2030, the ordinance is projected to continue to generate additional revenue of approximately $50 million annually.1

The Backstory

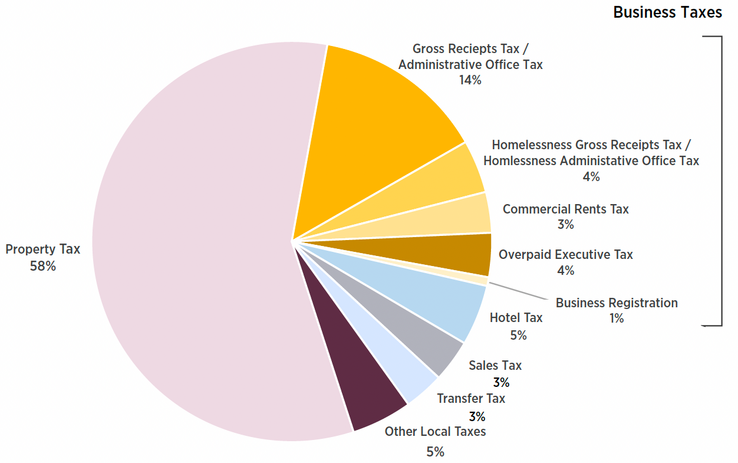

San Francisco collects about $1.4 billion per year in business taxes. Business taxes are the second-highest revenue source for the city, exceeded only by property taxes.

City Tax Revenue by Tax, Fiscal Year 2022–2023 (Total: $5.8 billion)

In 2012, San Francisco underwent major business tax reform when voters approved the city’s transition away from a payroll tax to a gross receipts tax, a change prompted in part by the Great Recession. The flat payroll tax fluctuated with economic cycles, and it disincentivized hiring because the tax increased as businesses grew their payroll. In contrast, gross receipts taxes are generally more stable and predictable over time. As a progressive tax, the gross receipts tax rate increases on the basis of gross revenues (as the California income tax does), which makes it fairer for small businesses than a flat payroll tax.

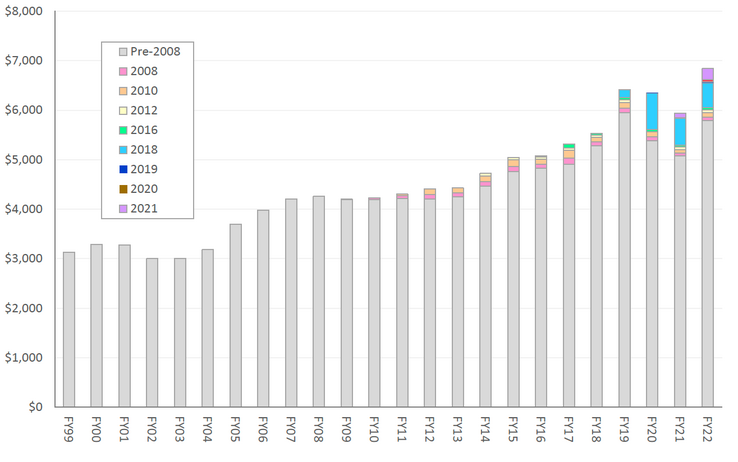

In the last six years, voters have passed additional ballot measures to increase gross receipts taxes. The Homelessness Gross Receipts Tax, which passed in 2018, imposes an additional gross receipts tax on companies with revenues greater than $50 million. The Commercial Rents Tax, which also passed in 2018, is a gross receipts tax on income from commercial leases, primarily offices, to fund child care and education. The Overpaid Executive Tax, which passed in 2020, imposes an additional tax on the annual gross revenues of companies where there is a large difference between the earnings of the top executive and the pay of the median worker in San Francisco. In addition to becoming the highest-tax jurisdiction in the Bay Area, San Francisco now has a very complex business tax structure with more than 14 categories and tiers.2 The chart below shows the growing number of taxes that have been approved since 2008.

Per Capita, Inflation-Adjusted San Francisco Tax Revenue by Year of Tax Approval

According to the controller, in 2022 the five largest taxpayer firms paid 24% of San Francisco’s total business taxes.3 By comparison, in 2012 the five largest companies paid 7% of the city’s total business taxes, illustrating that larger companies had been paying less than their fair share.

The rise of remote work has exposed some of the vulnerabilities of the existing business tax structure.4 For many industries, the city calculates the business tax owed on the basis of how many workers are employed in San Francisco. Under this “payroll apportionment factor,” the tax is reduced when employees work remotely outside of the city. Since the COVID-19 pandemic, the number of workers in the office has shrunk considerably, especially in tech and financial services, and the city is collecting lower revenues from the very firms that make up a high share of the city’s overall gross receipts. Remote work has also lowered the value of commercial office buildings in San Francisco, reducing the amount of Commercial Rents Tax, property tax, and real estate transfer tax revenues that the city can collect.

In addition, the climate for small businesses in San Francisco has become increasingly challenging. The current business tax structure exempts 85% of businesses because they have gross receipts less than $2.19 million, but many small businesses, including restaurants, fall above this threshold. In a recent analysis, the controller found that the city’s registration and licensing fees disproportionately burden small businesses, especially restaurants and bars.

In 2023, Mayor London Breed and Board of Supervisors President Aaron Peskin requested that the controller and the treasurer study potential tax reform recommendations that could serve as the basis of a November 2024 ballot measure. In February 2024, the Office of the Controller and the Office of the Treasurer and Tax Collector released a report with their recommendations.5 After significant engagement with businesses and community stakeholders, they finalized these recommendations in May 2024.6 Business groups, nonprofits, and labor organizations collected signatures for a ballot measure to implement the recommendations. Prop. M is the result of this collaborative process.

As an ordinance, Prop. M requires a simple majority (50% plus one vote) to pass.

Equity Impacts

Small businesses provide pathways to economic security for many low- and middle-income entrepreneurs, including Black, Indigenous, Latinx, and Asian entrepreneurs and their families. The proposed reductions in gross receipts taxes and fees for small businesses would help assist small businesses that have struggled to recover from the effects of the COVID-19 pandemic.

If Prop. M allows the city to become more economically resilient and stabilize its revenues, this would protect available resources for vulnerable populations.

Pros

Prop. B would cut taxes for many small businesses, providing some financial relief for those businesses that have struggled in the aftermath of the COVID-19 pandemic.

The progressive tax structure would shift the tax burden to medium, large, and wealthier businesses, injecting more fairness into the system.

The majority of businesses would be unaffected or only slightly impacted by the policy change.

The proposal was vetted with a diverse group of stakeholders over months of policy analysis and engagement and has wide-ranging support.

Cons

In the short term, this measure would have a slightly negative impact on city revenues.

SPUR's Recommendation

San Francisco is far too dependent on a small number of businesses for its business tax revenues. Moreover, the city’s high tax burden on certain industries has become a liability, as there is a chance that those businesses could move away or reduce their footprint in San Francisco. This measure promises to build a more resilient and transparent tax system in San Francisco, while providing tax relief to small businesses that have struggled to recover from the pandemic. The measure would be fiscally neutral over the long term and would improve the city’s financial footing. It would protect dedicated funding for critical priorities like homelessness services, while simplifying a highly complex tax structure and creating more predictability for the private sector.